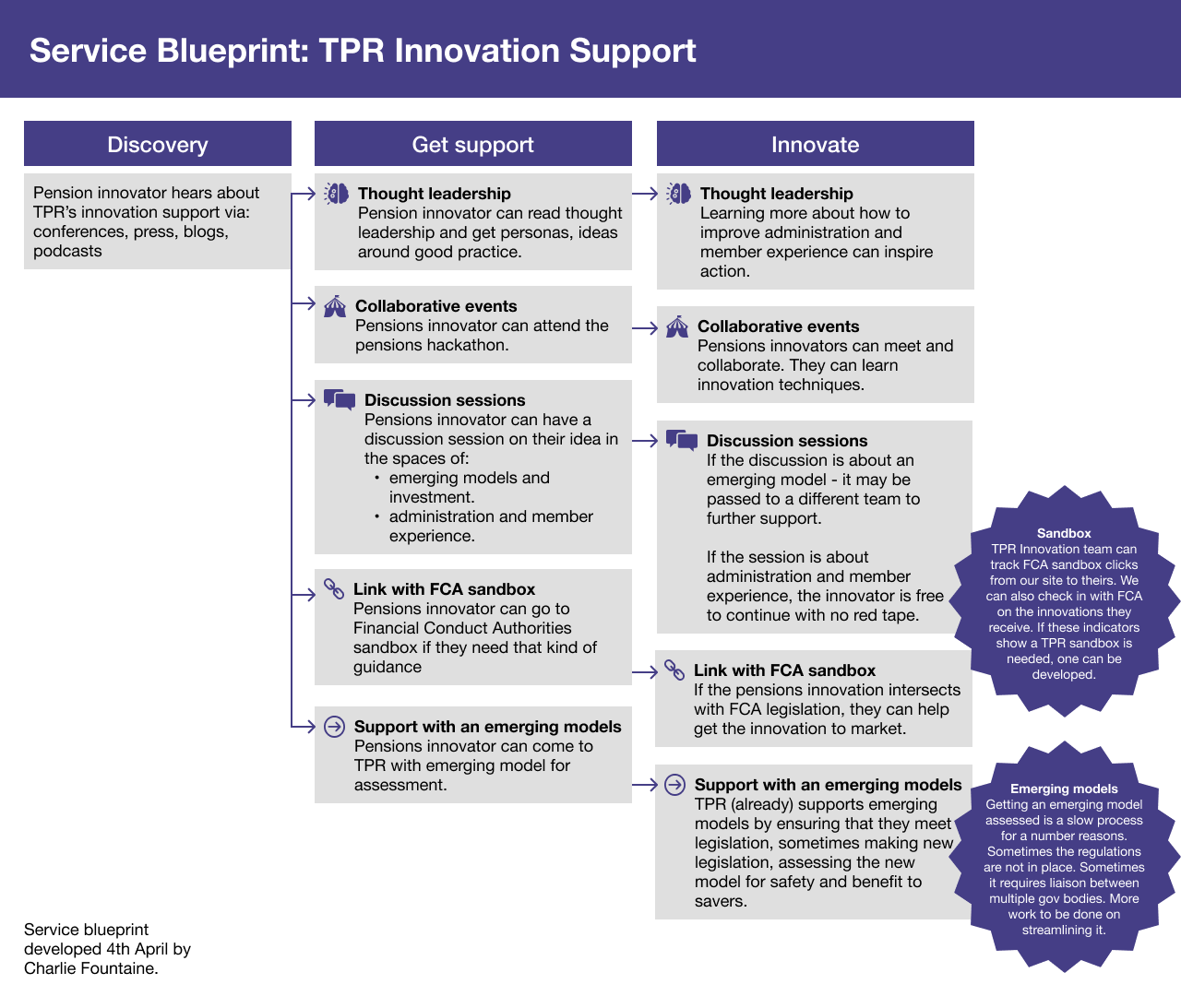

Get support with your pensions innovation

In November 2024, Sir Keir Starmer, the Labour Prime Minister asked all UK regulators to focus on stimulating growth in the economy. My challenge was to work with The Pensions Regulator to understand how we could drive innovation in the pensions industry.

I led a multidisciplinary team, including pensions experts, through discovery, alpha, beta and live. We developed The Pension Regulator’s innovation support service.

I led the research with external pension schemes and firms, and internal pensions experts at The Pensions Regulator. I aimed to understand how we could boost innovation in the pensions industry.

Through the research we uncovered 2 main innovation areas within the UK pensions market:

Investment and emerging models covers new ideas and solutions relating to the way a pension fund invests, including the model that underpins it. This includes: master trusts, superfunds and collective defined contribution schemes (CDCs). In the UK, there is currently 1 superfund, and 1 collected defined contribution scheme. The UK government encourages innovation in pension models, to drive greater gains for UK savers. The Pensions Regulator has a role in assessing these new models, to ensure they are in the benefit of pension savers.

Administration and member experience covers anything that savers interact with. Pension web and phone apps. Pension communications. Allowing savers to be able to see their balance, change their details when needed. Some pension schemes have neglected member experience, which has an effect on the amount that people save. When people are not engaged with their pension, they save less. Therefore innovation in this space would benefit savers directly.

From the research, we were able to understand the barriers to pension innovation.

“If someone came with a scheme design that just wasn’t sensible at all, the regulator could say we’ve looked at it and we’re not going to authorise it because there’s this problem with it and you need to think again.” Participant 3.

Multiple participants talked about it being helpful to have an early, informal conversation with the regulator to understand how to move forward with a pensions innovation, without breaching the rules.

“Really helpful in showing that this is how a particular innovative development worked. This is how the employer handled it. This is how the trustees handled it, and this is how the regulator made sure that it was fit for purpose. And improved outcomes for savers. A case study is worth 1000 slides…”

Participants wanted to be able to learn from each other, and read case studies in relation to pensions innovation. This was one of the most popular ideas during value proposition testing, with pensions innovators saying they already looked for this kind of information online.

“Big old schemes that have been running for years and years, you might want to automate. Member transfer values. You might want to automate retirement quotes. But if the data underlying it is terrible, it’s not going to make sense.. It will just give you nonsense answers because the data is wrong.” Participant 2

Is a barrier to improve membership experience and administration, and we know that a good experience can improve saver outcomes.

“We were bombarded with a lot of detailed questions. Telling us what we had to do instead of exploring what we could do.” Participant 8

“It was one of those organic processes where you don’t really know how it’s gonna go and where it’s going. You just focus on the immediate next stage of the next month and fix that issue…” Participant 3

We learned that the process for getting an emerging models approved was slow and unclear. Both internal participants from the regulator, and external pensions innovators struggled with the lack of process.

We developed a simple, lean service to support pensions innovators in the market. This service includes:

Pension innovators can request a discussion session in the early stages of developing a new pensions idea or solution. They meet with The Pension Regulator experts to discuss their pensions innovation. This is important because there are pension innovations that are so new - current regulation may not cover them, and our research showed that an informal chat with an expert could allow them to develop their innovation. During the project we began to pilot the discussion sessions, including the triaging system at The Pensions Regulator that supports it. We then launched the offering in May 2025.

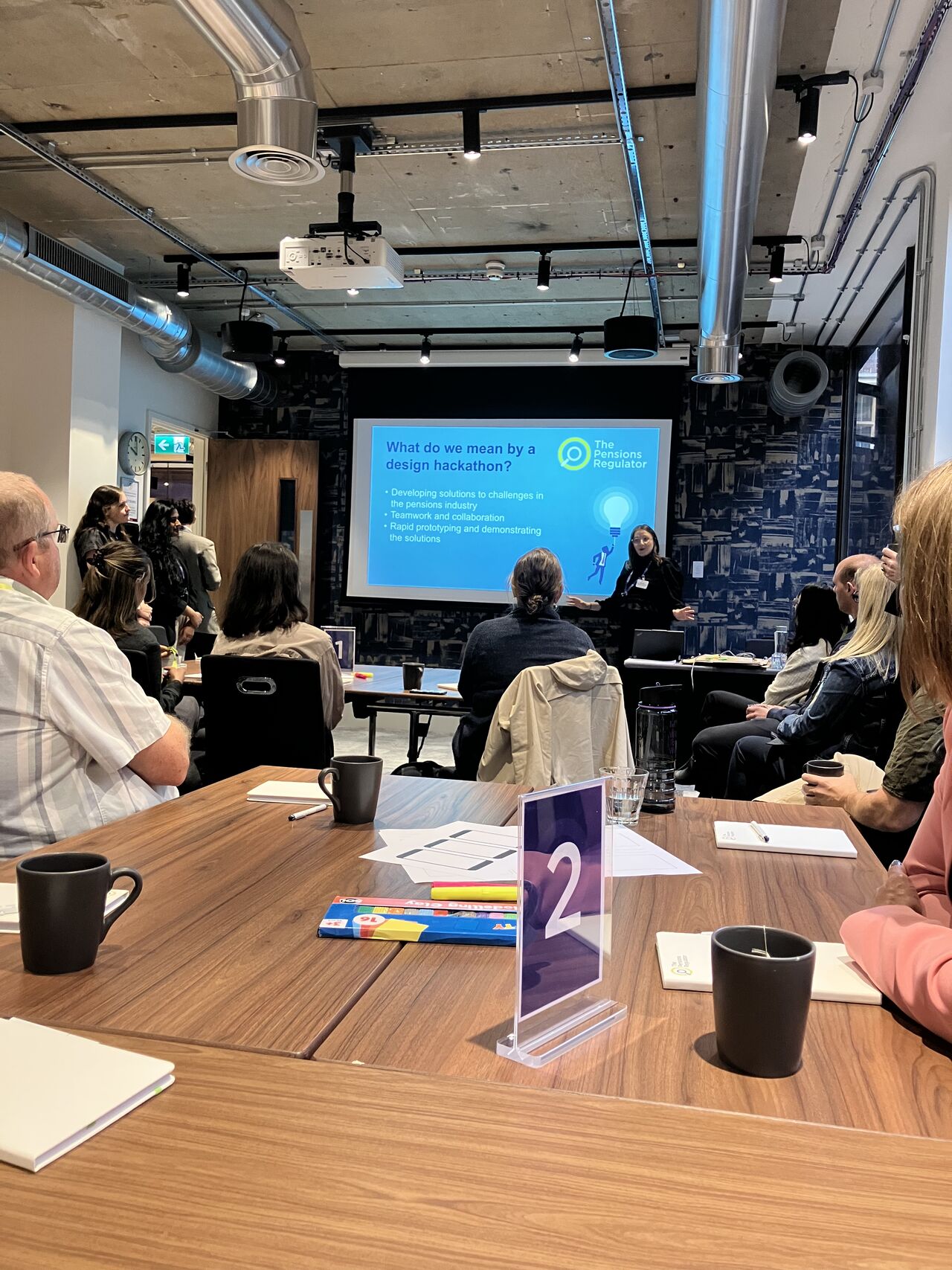

Collaborative events include things like hackathons: allowing pension innovators to make connections across the industry. We learned in research that pension innovators had key challenges that were shared across industry, that they were willing to collaborate on. During the project we had our first pensions hackathon June 2025.

Blogs, reports, information on good practice in pensions innovation was something that was popular with participants during research and testing. They wanted to get regulators stance on key topics like; targeted pensions support, guided retirement and more.

Instead of creating another sandbox, we developed a partnership with FCA’s innovation lab. This cross-government working meant that pensions innovators would be able to go to FCA for regulatory and data sandbox support.

The regulator already supports new pensions models, for instance superfunds. We learned from research that we needed to streamline the process for supporting emerging models. We developed a brief and project plan for this work to take place. In April 2025 The Pensions Regulator announced that they would be taking the plan forward to streamline the process for supporting emerging models.